|

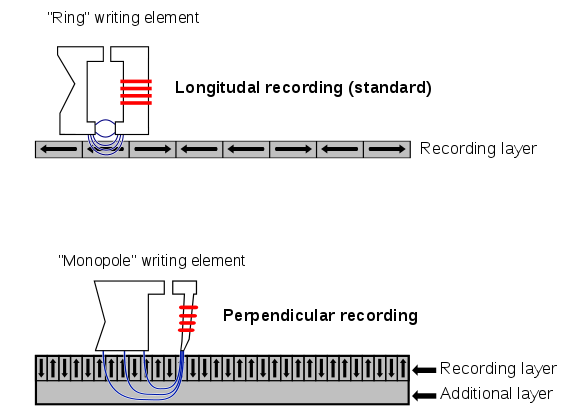

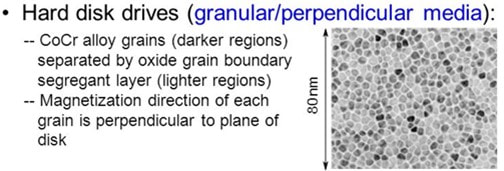

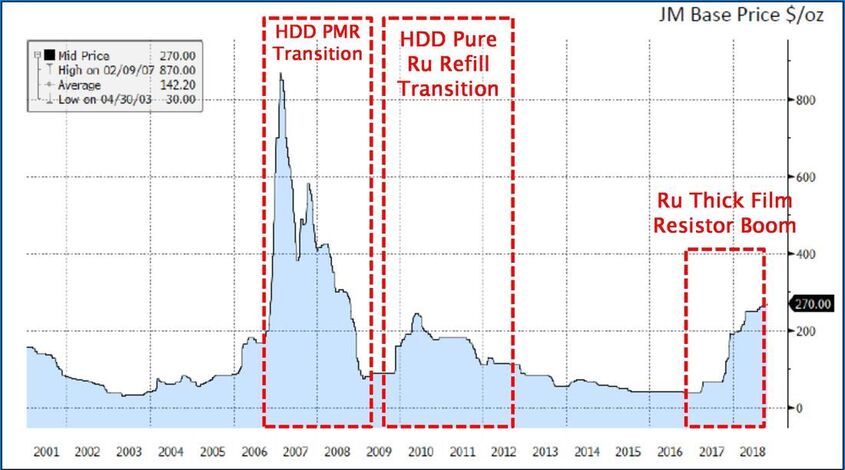

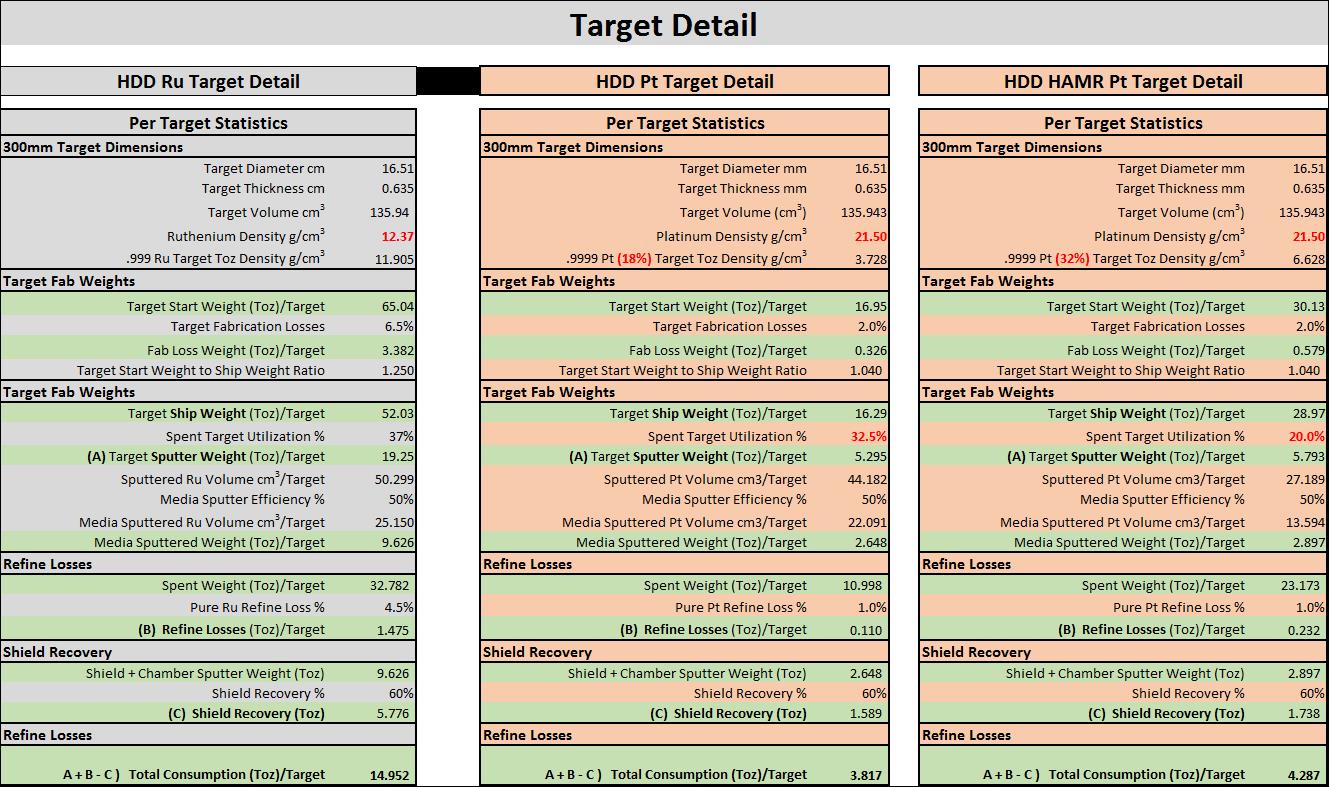

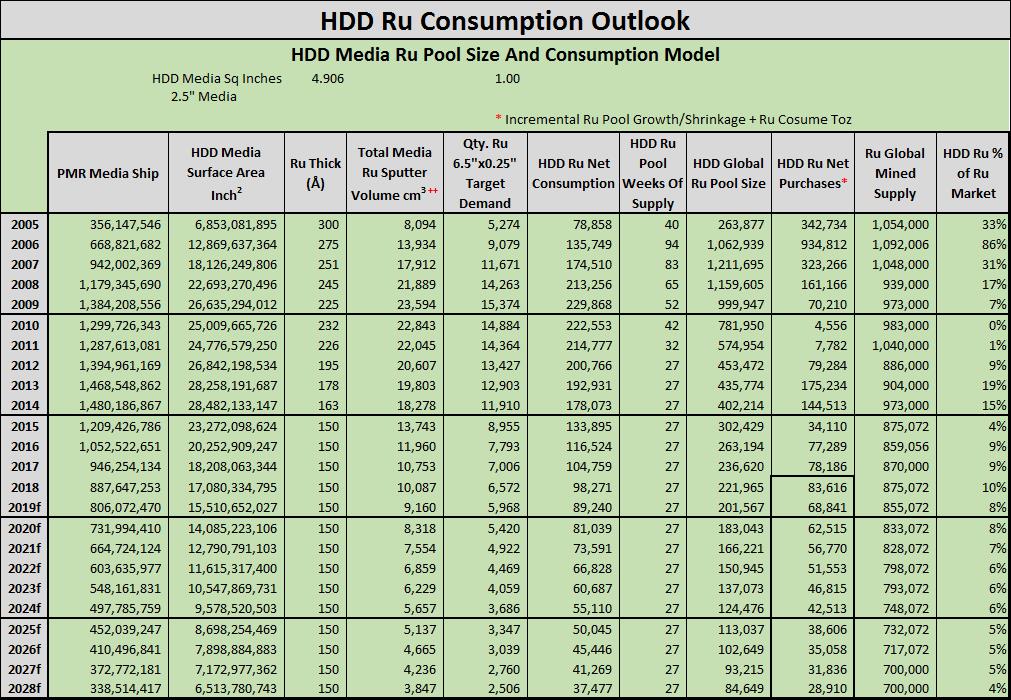

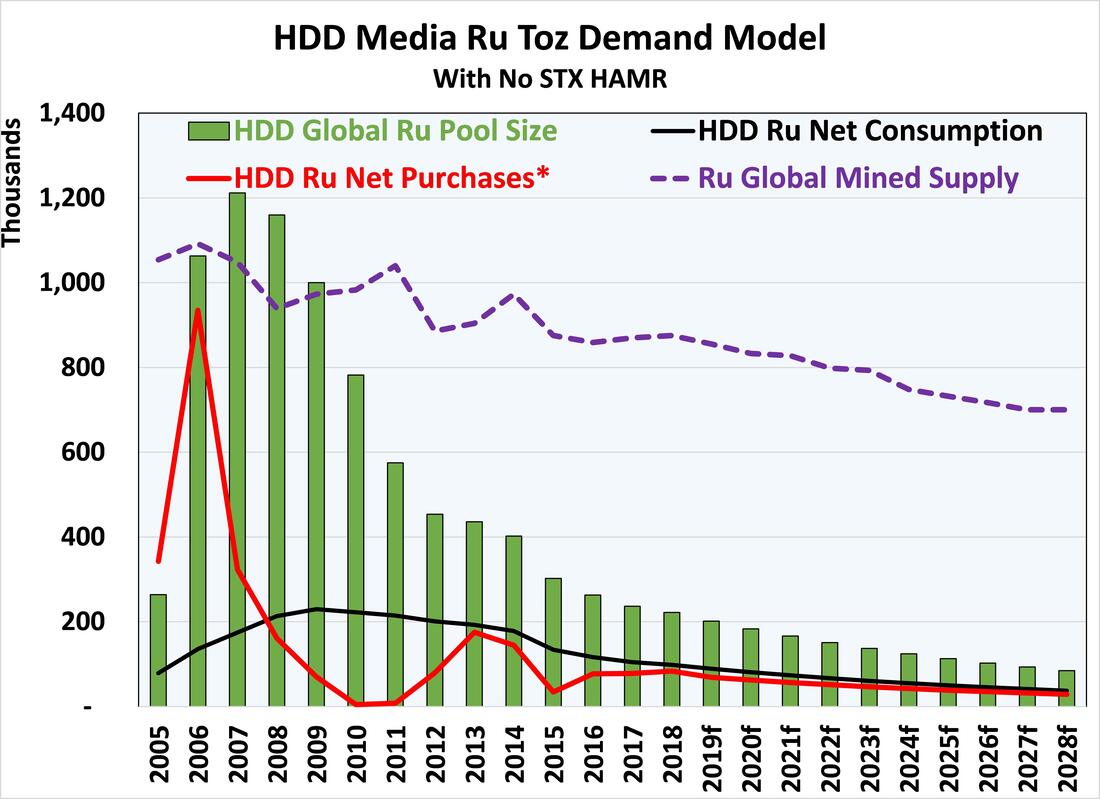

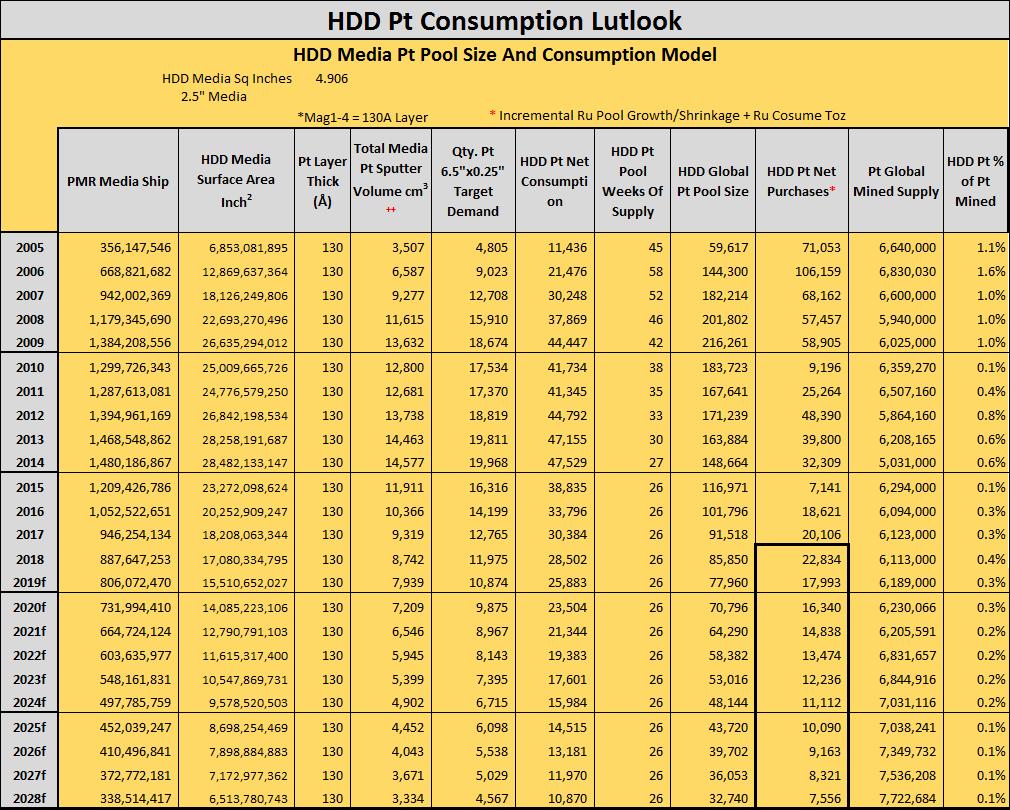

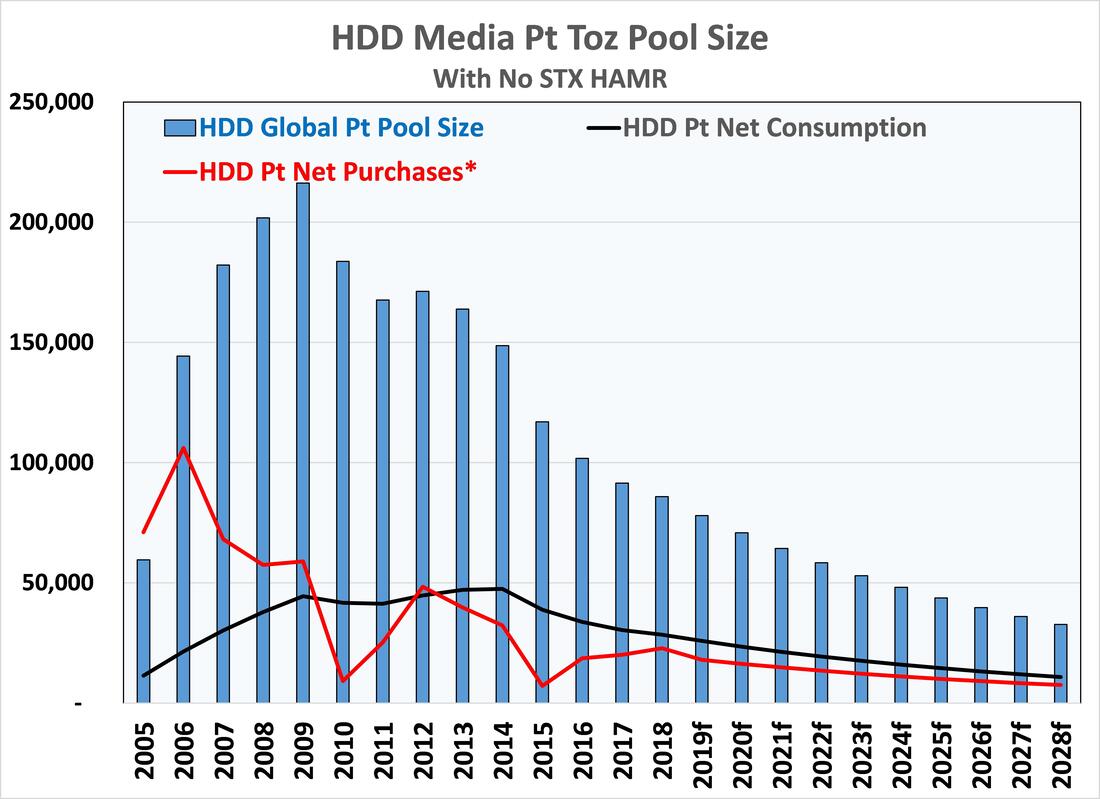

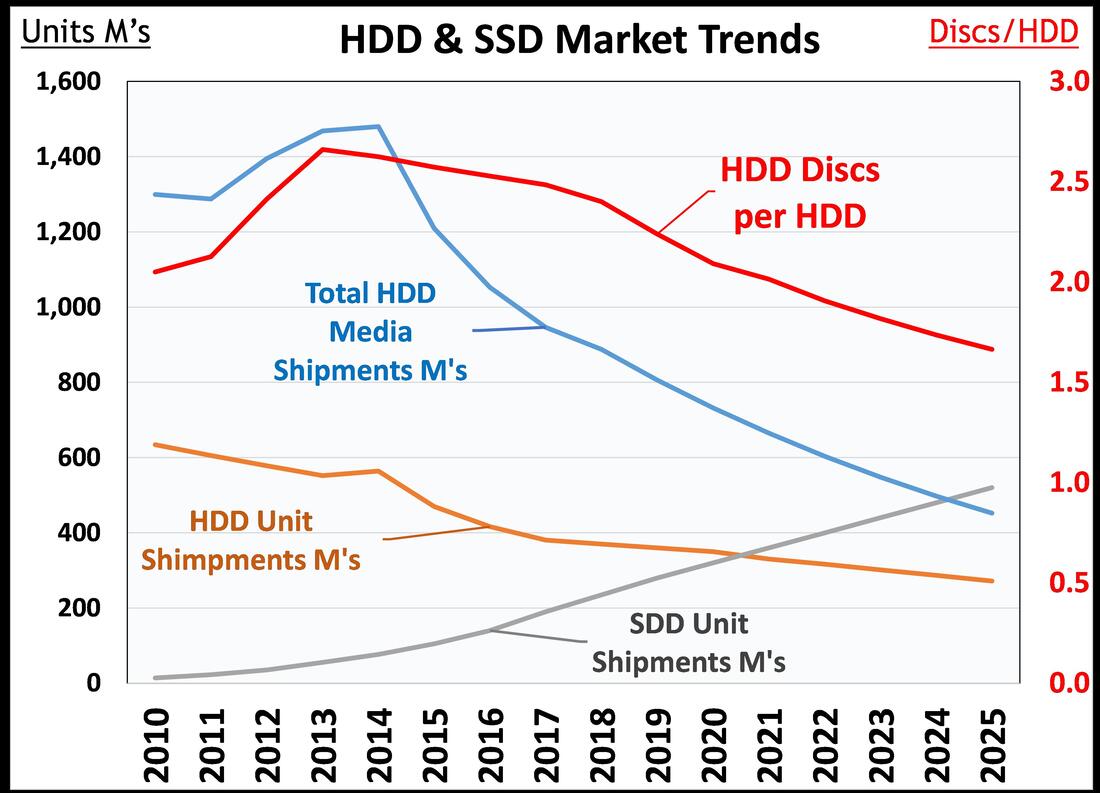

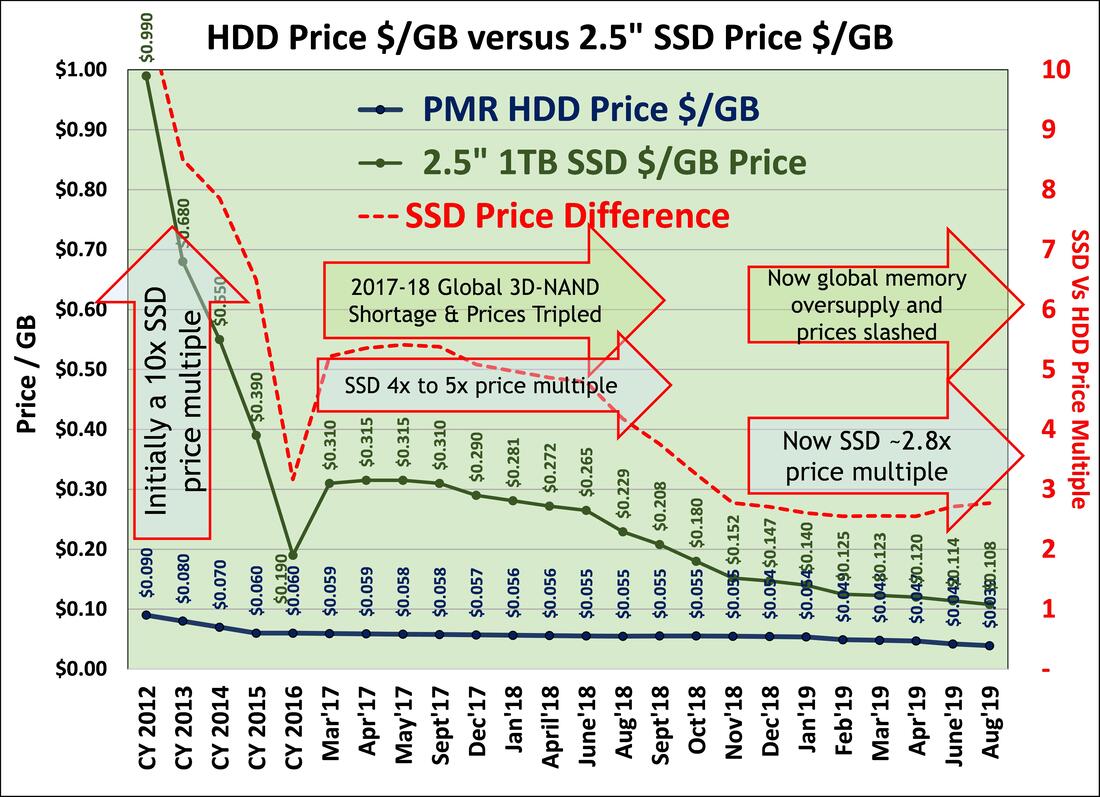

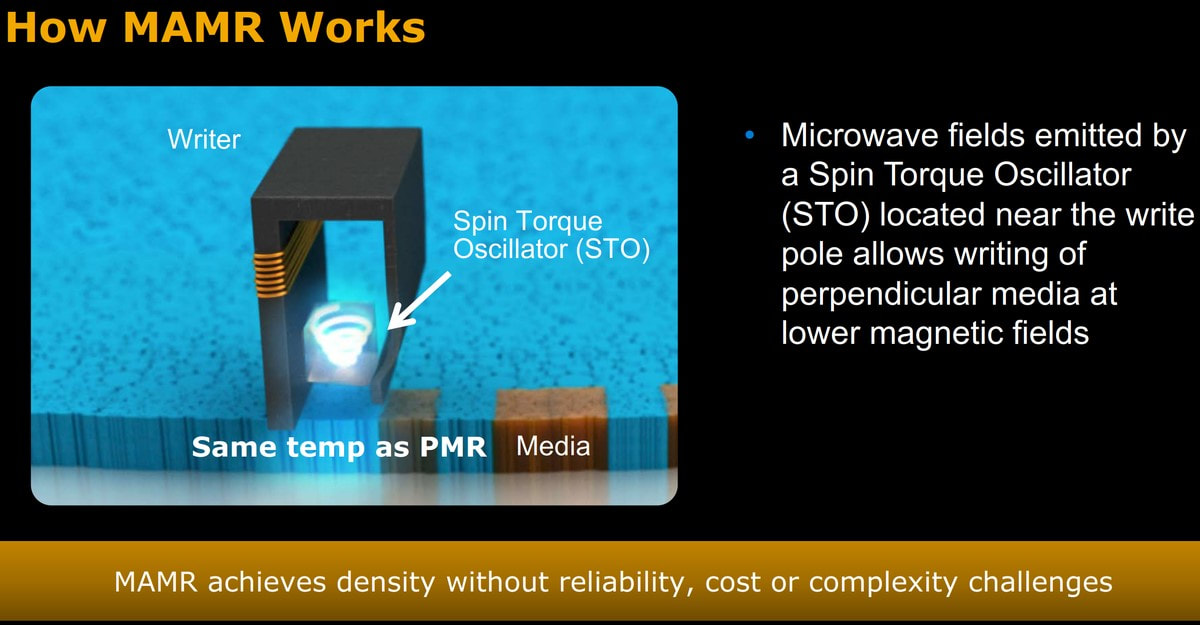

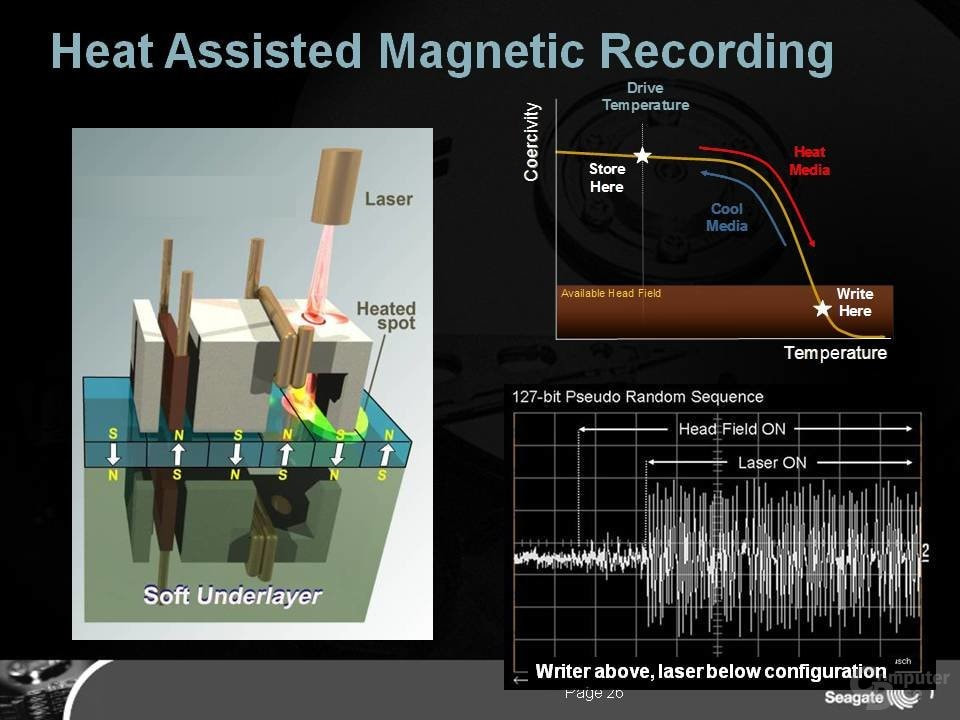

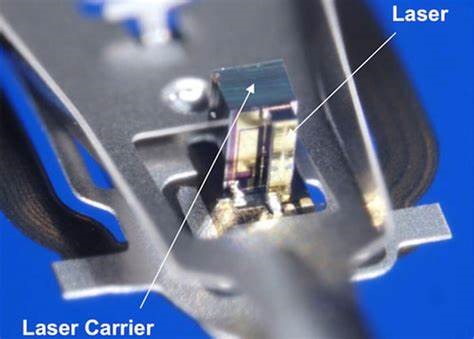

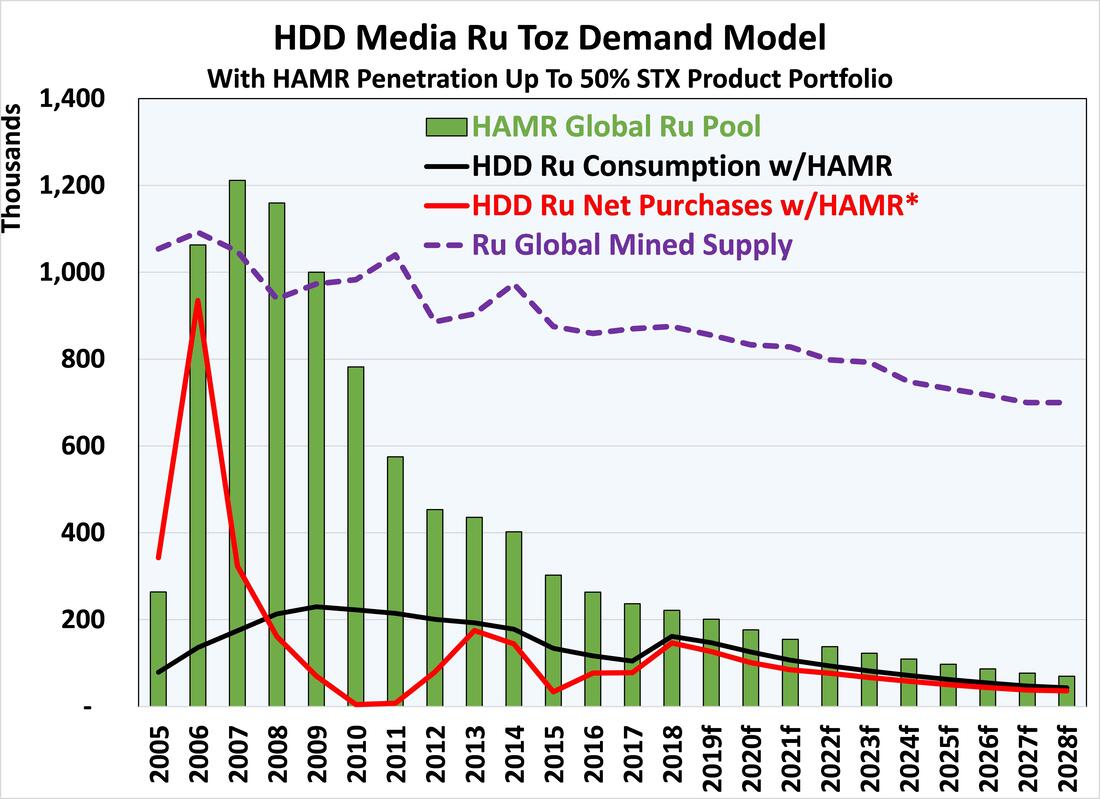

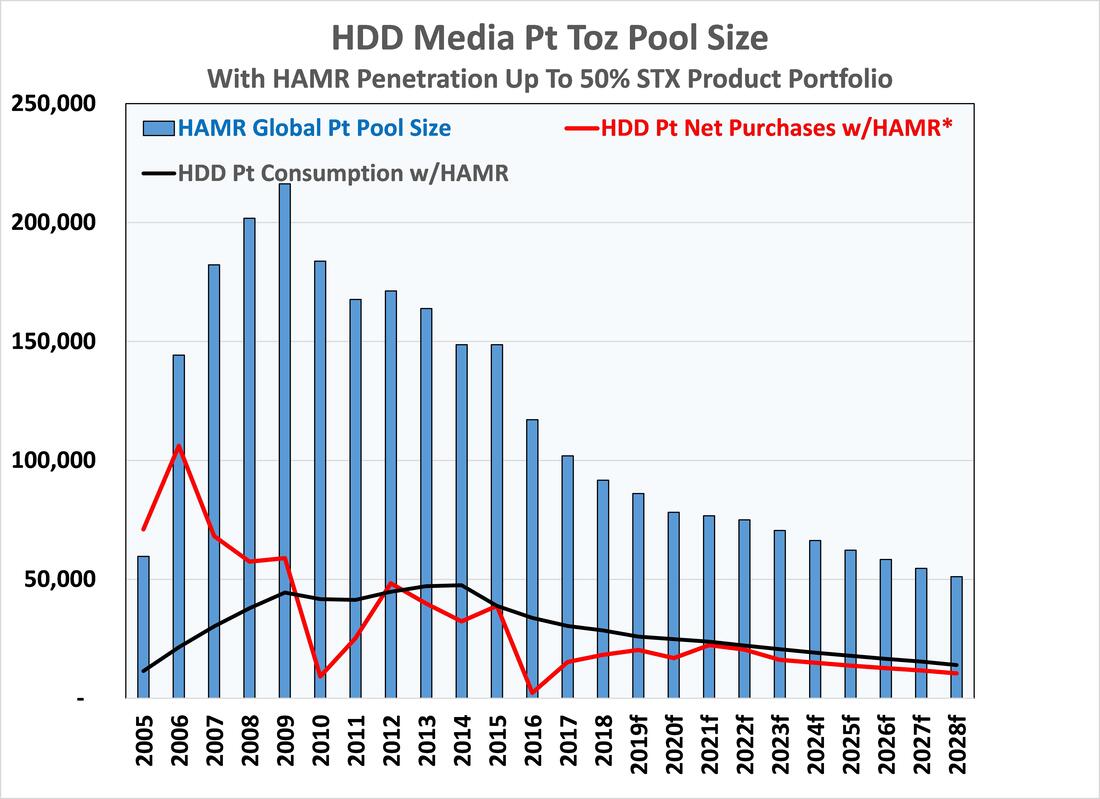

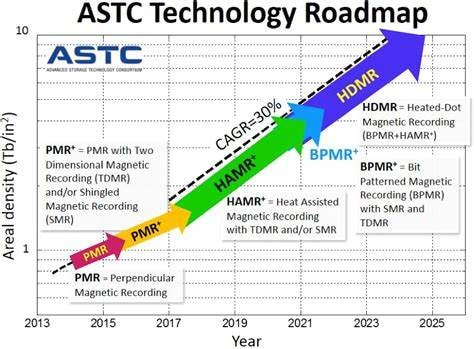

The Hard Disk Drive Industry PMR Transition 2006-2008 The Hard Disc Drive (HDD) industry has enjoyed a 50+ year lifespan. HDD’s have enjoyed multiple significant technology transition during that 50+ year span. One of the most dramatic technology transition by the entire HDD industry was a transition from Longitudinal Recording, to today’s Perpendicular Magnetic Recording (PMR). The use of Ruthenium layers on the media had a transformative impact on the bit density of the data stored on HDD’s. The HDD industry shocked the PGM market starting in 2006-2008 with a huge demand for Ruthenium PVD Sputtering Targets to sputter these layers of ruthenium on the media to enable this higher density HDD. The yield impact of this technology on a per drive basis was huge, over $2/HDD in drive yield benefit. Executives throughout the HDD industry could not transition their entire product portfolio’s quick enough to this new recording technology. The impact on the Ruthenium market was profound.  Longitudinal versus Perpendicular Recording Diagram Sputtering a layers of Ruthenium under the following multiple Platinum-Chrome-Cobalt magnetic layers provided columnar magnetic layer growth, allowing for dramatic areal density increases.  Perpendicular Granular Media Grain Structure The long term Ruthenium price history is plotted below. You can see the annotation for HDD PMR (perpendicular). The HDD market went from very low amounts of Ruthenium Demand to being over 80% of the global Ruthenium demand for the next 3-years. Finally starting in 2009, the HDD industry had saturated their Ruthenium Sputter Target pool accounts, and were off driving a series of thrifting actions including reduced Ruthenium Layer Thicknesses, alloying for reduced Ruthenium, and a technique called Ruthenium Refill, essentially taking a spent pure Ruthenium target and instead of returning to 65% of the unused weight back to refine, re-press the spent target with some additional fresh ruthenium, and repress the target back to its original shipped/new conditions. This dramatically accelerated the target life cycle. That coupled with Ruthenium secondary refine optimization, refine cycle times were reduced from over 90 days to 21 days. All of these actions compressed the weeks of supply needed to support the same media volume. By 2011, the HDD industry was < 20% of the global ruthenium demand, buying only new ruthenium to top off its pool accounts and replace consumption onto the product.  Ruthenium Long Term Fix History – BASF IB USA Price/Toz HDD Ruthenium and Platinum Target Detail Target Detail Includes Precious Metals Start, Ship and Spent Weight, Target Utilization, Refine Losses and Total Shield and Target Recovery Toz, for a Final Net Toz Consumption per Target.  Ruthenium and Platinum (PMR) and FePt (HAMR) Target Model Assumptions Ruthenium HDD Industry Demand Model A model is then created to transpose the media demand, into Ruthenium Target demand, to Ruthenium Pool Size Requirements, to Ruthenium Consumption, to Ruthenium Net Purchases year over year.  HDD PMR Ruthenium Model HDD Industry Ruthenium pool sizes peaked at about 1.2Moz in 2007, at the height of the Perpendicular Recording transition. Secondary Ruthenium Refining capacities were still be added, and Pool Account saturation had been achieved. Net Purchases of new ruthenium for HDD Industry pool accounts peak in 2006 at over 930koz. This amount on its own exceeded mined production. Only through the processing of previous years mined surplus concentrate was the overall global demand met. As you can imagine, the price of Ruthenium had skyrocketed to nearly $800 Toz, up from a slumbering $70 before this HDD surge in buying. HDD Ruthenium demand today is about 10% of the overall mined annual ruthenium. Ruthenium HDD industry Demand Model Summary Here is a graph illustrating the overall industry Ruthenium pool account sizes, against the context of the mined supply. Also shown in the chart in the Red Line is the HDD Industry net ruthenium purchases to meet that peak demand and pool account saturation.  HDD Industry Ruthenium Demand Model (PMR) HDD PMR Platinum Demand Model A model is then created to transpose the media demand, into Platinum Target demand, to Platinum Pool Size Requirements, to Platinum Consumption, to Platinum Net Purchases year over year. Again this table capture the number of Pt Magnetic Layer targets were in demand. Recall that as opposed to Ruthenium, which was a very high composition of 100% Pure Ru for over half of the targets, or RuCr or RuCo alloys with 80% ruthenium. The Platinum targets were often lower in platinum content in the range of 14%-20%. Therefore the total Platinum requirements were lower than Ruthenium.  Platinum HDD Industry Demand Model Platinum HDD Industry Demand Model Summary The Platinum peak industry pool account size was around 218 koz in 2009. The peak net annual purchase was around 108k or 1.0% of the mined supply in 2006.  HDD Industry Pt Requirements Solid State Drives Now the most threatening issue to HDD’s, a rotable memory recording device with hundreds of moving part, is a fully solid state drive filled with NAND Flash Memory instead of a rotable magnetic dis and recording heads. SSD’s are threatening HDD’s existence. Just 20 year ago there were over a dozen HDD manufacturers. Today there are three, Western Digital, Seagate, and Toshiba. 20-years ago there were 20 media manufacturers, today there are four. Western Digital (including HGST), Showa Denko (independent), Fuji Electric (Seagate captive) and Seagate Technology. Hard Disc Drives versus Solid State Drives The current market is under some assault from a new technology Solid State Drives (SSD). SSD’s are based on 3-NAND memory, operate faster, access data faster, but come at a significant price premium. The current HDD and SSD market trends look like this. HDD overall unit shipments are declining. Not shown but Exabyte’s of HDD memory are actually increasing. The HDD’s areal density is increasing faster than the unit decline, such that the overall HDD Exabyte’s shipped is increasing with few drives. The media (or HDD platter that contains the data) shipment volume is also declining, and the average HDD discs per drive is also reducing.  HDD Vs SSD Market Fundamentals Media Demand = Precious Metals Demand. What is also key to note is that the HDD Media Shipments are declining. The number of recording heads per drive matches the number of media surfaces in most drives. This is key to the precious metals demand, is the media, not the heads. The media contains approximately 98% of the Platinum and Ruthenium used in magnetic recording. Note: This excludes the HDD and SSD’s printed circuit boards and components, which in terms of e-waste is actually some of the most precious metals rich containing electronics that is out there. As for the media, since the fundamental film structure thickness have settled down, now only compositions of Platinum and Ruthenium alloys changes, not the overall thickness of the magnetic layers on the media. SSD shipments can be seen increasing. The SSD shipment volume should match or exceed that of conventionally rotatable memory by 2020-2021 time frame. SSD’s as it ends up are faster, preferred many of today’s data centers Artificial Intelligence operations. SSD’s do have limitation on the number of times you can successfully re-write data to the same device, where HDD’s are fairly limitless number of re-writes. SSD’s however are more expensive than HDD’s, making HDD rotatable memory the preferred media for many data centers, especially those that focus on video content, the largest amount of data stored. The SSD vs HDD Cost per GB is expressed in the following chart: Initially SSD’s were 10x higher in price than rotatable HDD memory. From 2012, that SSD price multiplier dropped down rapidly with 3D-NAND expansion in the marketplace to about 3x in 2016. 10x to 3x in 4 years. Then global demand for consumer electronics and smartphones taxed the global flash memory marketplace. Almost overnight, Flash Memory prices for SSD’s nearly tripled in 2017 and early 2018. It wasn’t until there was further expansion of 3D-NAND and more complex layering processes (up to 96-layers) that the industry overall supply picture once again exceeded global demand. A flattening of the smartphone global unit demand also fed this oversupply situation. Suddenly again, Flash Memory price wars are in full swing. SSD are enjoying a best every 2.5 to 2.8x multiple compared to HDD prices.  HDD Vs SSD Retail Price per GB Shopping 1TB 2.5” drives for both – Lowest monthly price point on Amazon One Last HDD Technology Transition So in order to compete on cost with this SSD price premium, HDD’s need to take additional steps to lower the cost per GB. There are actually two sets of technology that are being deployed. Western Digital and Toshiba has recently rolled out MAMR, Microwave Assisted Magnetic Recording HDD’s. Seagate is taking a much more dramatic design change to their media and heads once again rolling our HAMR, Heat Assisted Magnetic Recording. MAMR uses the same perpendicular media film structure. No changes to the Ruthenium and Platinum layers, use, or consumption per disc.  HAMR, Heat Assisted Magnetic Recording HDD’s last technology transition will be by Seagate in the form of HAMR, Heat Assisted Magnetic Recording. This is a much more dramatic technology transition. The Recording heads incorporate laser to heat the media magnetic layer to write the data. The media platinum film structure changes from a PtCoCr (Platinum, Cobalt, and Chrome) based alloy and structure, to FePt (Iron Platinum) based film structure. Platinum composition increase. Taking into account film structure thicknesses, Platinum loading swill increase 1.7x over perpendicular. However, there is zero, no Ruthenium in these FePt magnetic film structures. Below are a few technical executive summary slides from Seagate illustrating the HAMR Technology. The latest timing on Seagate’s HAMR is Seagate delivering HAMR CTU's by year end 2020, with a more significant commercial ramp in 2021. Seagate has been running small amounts of HAMR drives into a partner OEM just to better baseline the overall yield, reliability, and scalability issues with this technology jump.  HAMR Technology Summary - Seagate  HAMR Recording Head - Seagate Ruthenium HDD industry Demand Model Summary Using the same model we used to PMR, here are the reduced Ruthenium HDD Industry requirements when you shows Seagate with some 50% HDD global market share. Not HDD+SSD Seagate only has some 35% market share today, but WD and Toshiba have larger SSD portfolio’s leveraging on the WD-Sandisc and Toshiba Memory NAND product base. Also note the HAMR penetration will not be all of the remaining HDD’s. Laptops, Desktops and many lower HDD capacity drives will never adopt HAMR. HAMR is only intended to impact the highest capacity drives including Near Line and Enterprise. The hope for Seagate is the number of heads and discs per drive can be reduced, using fewer of the more expensive HAMR Recording heads and media. HAMR is a more expensive per disc and head technology that will nearly double the areal density. So instead of 6-7 disc 16TB- 20TB PMR drives, a 4 disc HAMR drive will achieve 2oTB initially. Laptops, Desktops and other smaller capacity requirement systems don’t need, and won’t use that muck memory. So again those lower capacity drives will stay on the PMR Technology.  Platinum HDD industry Demand Model Summary Platinum compositions in HAMR do increase. Overall Platinum on HAMR drives should be 1.7x more than PMR. Below is the modeled Platinum HDD Industry Pool Size, Consumption and Net Purchases.  HAMR Summary Impact to Ruthenium and Platinum Demand From 2018 through 2028 (11 years), HAMR is expected to reduce Ru Net Purchases by 282 koz. Since the HDD industry is already in a mode of consuming down its pool account positions, this is indeed a fairly small impact. For the same time interval, HAMR is expected to increase Pt Net Purchases by 34 koz. Could there be one more HDD Technology Turn? The short answer is no. For many years, the technology roadmap has shown beyond HAMR a transition to BPMR (Bit Patterned Magnetic Recording), where the grains or columns of platinum are produced with Litho etch processes. Beyond that HDMR (Heat-Dot Magnetic Recording), or Head Assisted Bit Patterned Media. Neither Seagate nor Western Digital are staging significant R&D resources for this very expensive and process/factory altering technology transition. It appears to most outsiders that the SSD encroachment on HDD is to immediate of a risk to warrant huge R&D and Capital Expense to a very dramatic technology change, even if it worked.  ASTC HDD Technology Roadmap Matt Watson can be reached at PreciousMetalsCommodityManagment.com MattWatson@PreciousMetalsCommodityManagment.com 1694 Cairo Street, Livermore CA, 94550 USA

9 Comments

8/19/2021 03:53:33 am

Hi, 8/20/2021 01:32:34 am

Hi, 8/21/2021 03:24:27 am

Hi, 8/24/2021 01:57:13 am

Hi, 8/24/2021 04:09:18 am

Hi,

Incredible posting this is from you. I am really and truly thrilled to read this marvelous post. You've really impressed me today. I hope you'll continue to do so! Also check into our site. https://hard-drives.co/toshiba-canvio-advance-1tb-portable-external-hard-drive-usb-3.0

Incredible posting this is from you. I am really and truly thrilled to read this marvelous post. You've really impressed me today. I hope you'll continue to do so! Also check into our site. https://hard-drives.co/seagate-external-hard-drive-not-showing-up-windows-10

Hi, It is such an excellent article, thanks for sharing this article with us. If you are facing any issues on hard drive, then follow the simple steps given in Leave a Reply. |

Author

Matt Watson, Precious Metals Commodity Management LLC Archives

November 2020

Categories |

RSS Feed

RSS Feed