|

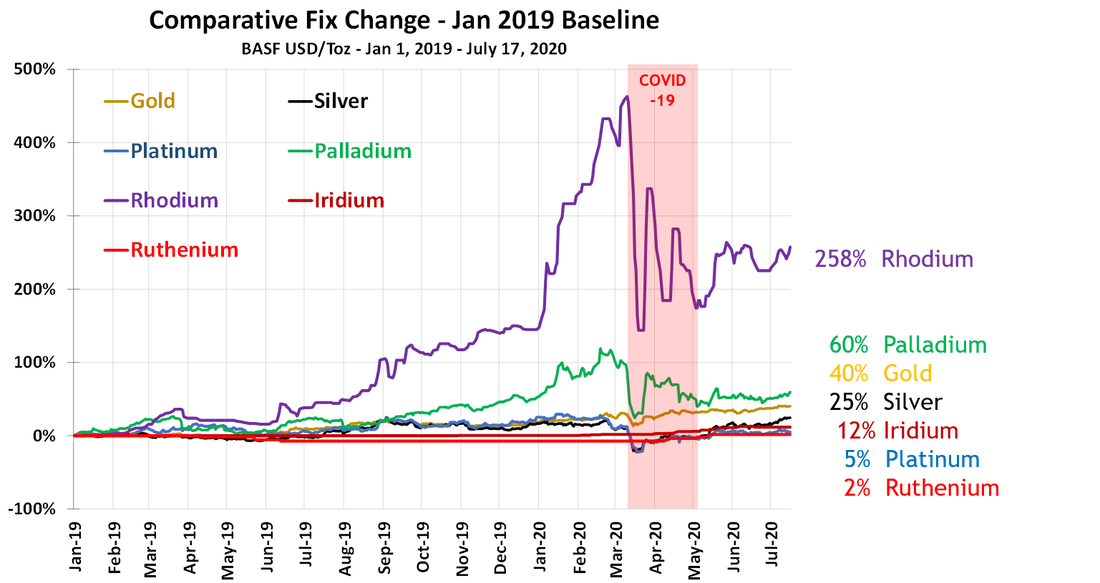

Basket Fix Comparison Since January 2019  Precious Metals Basket Since January 2019:

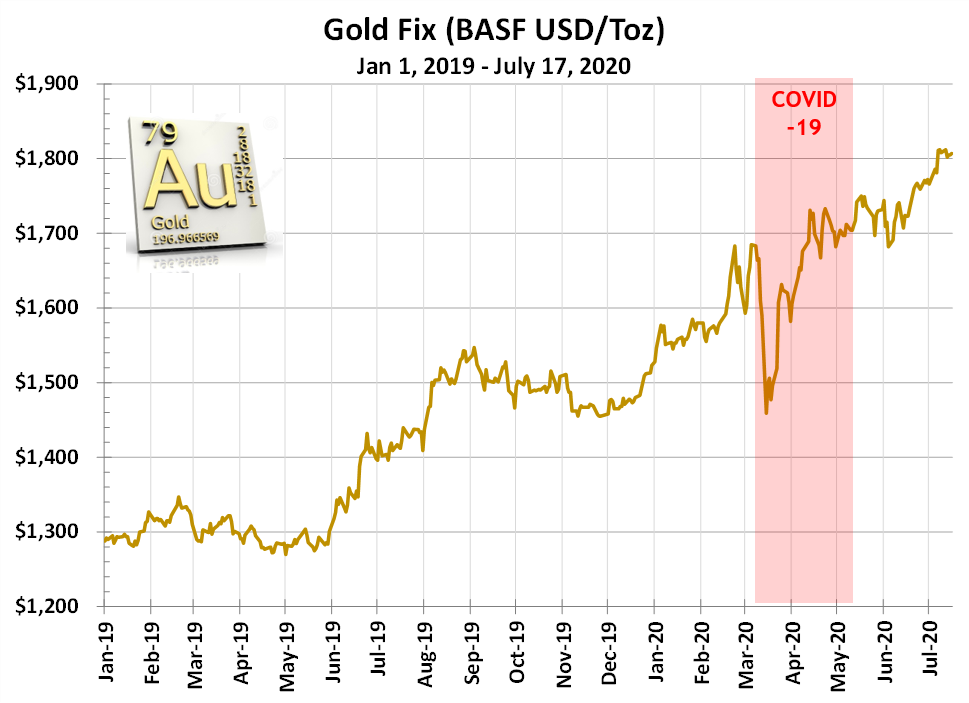

Let’s quickly look at each one and key ratios and relationships.  Gold

Supply Highlights: Gold is a finite resource who’s mined quantities will decline over the next decade. Demand Highlights:

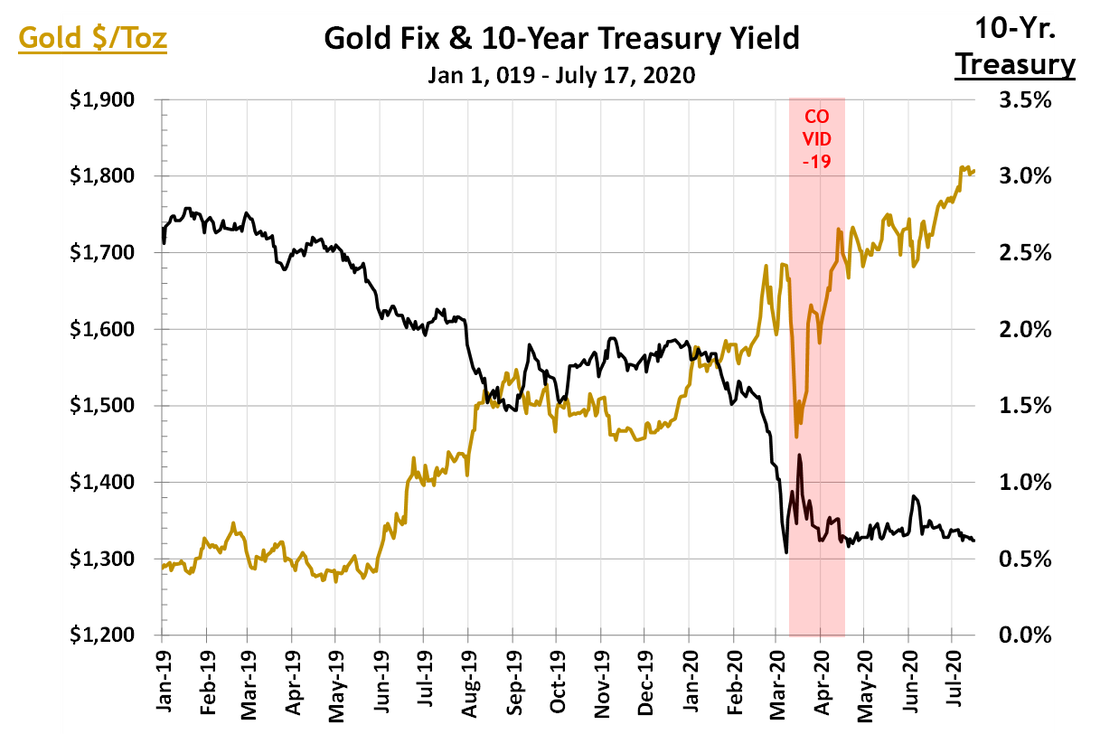

10-year Treasury Yield vs Gold Fix

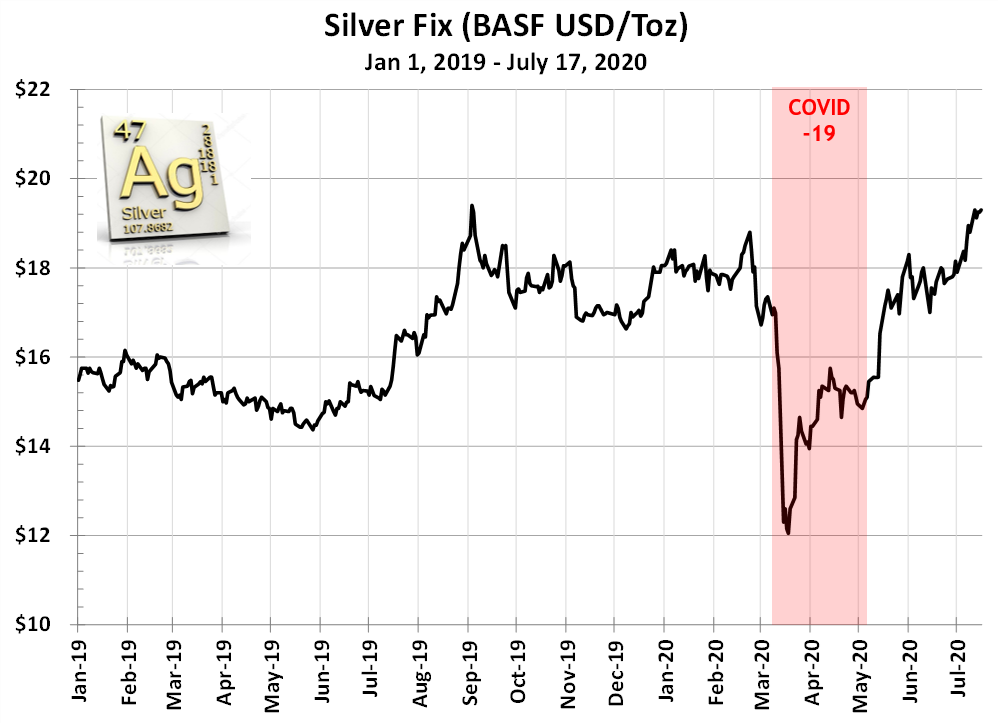

Silver:

Supply Highlights: COVID mining disruptions in numerous countries will continue in Q3/4 2020. Demand Highlights:

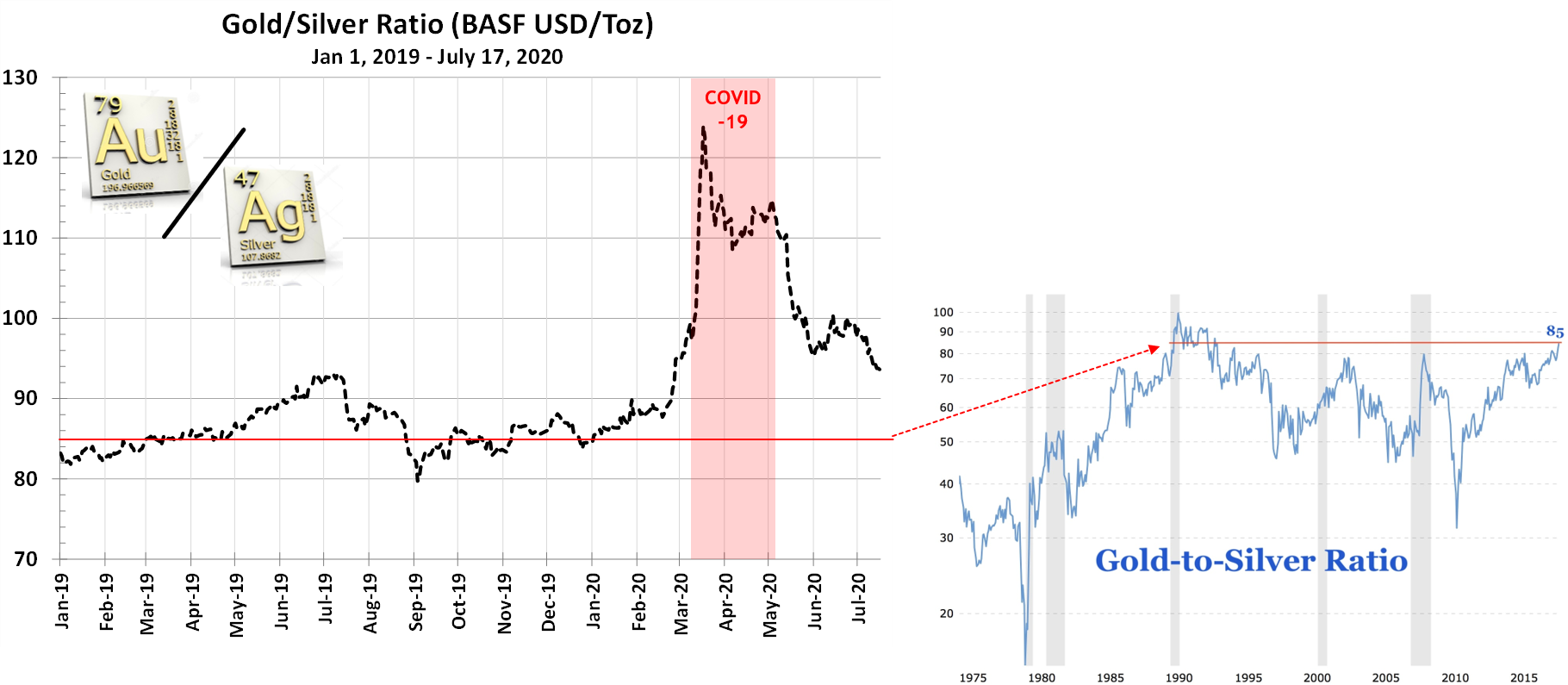

Gold/Silver Ratio

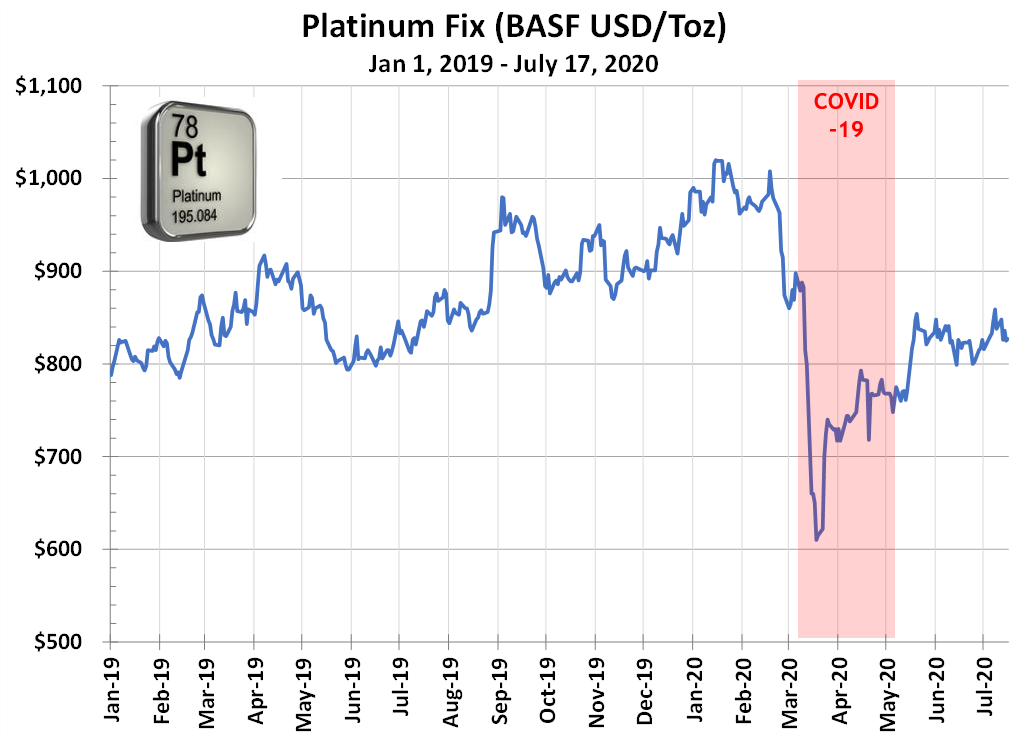

Platinum

Supply Highlights: Clearly COVID related impacts in 2020 will limit supply. Demand Highlights:

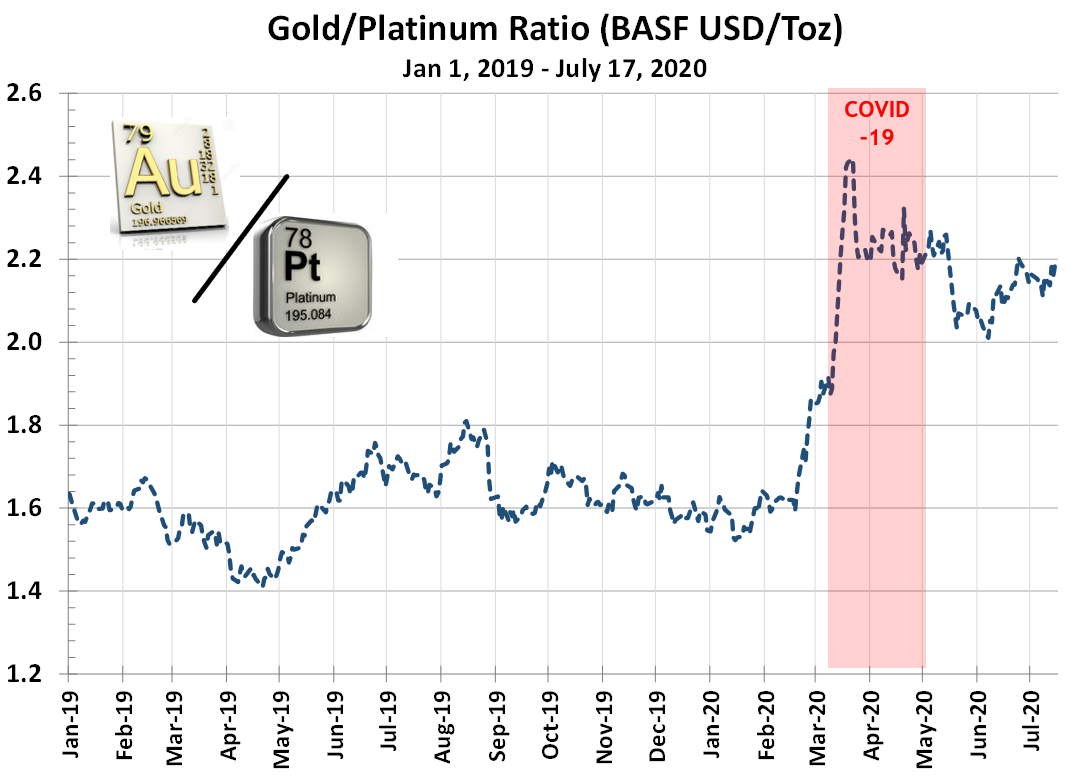

Gold/Platinum Ratio

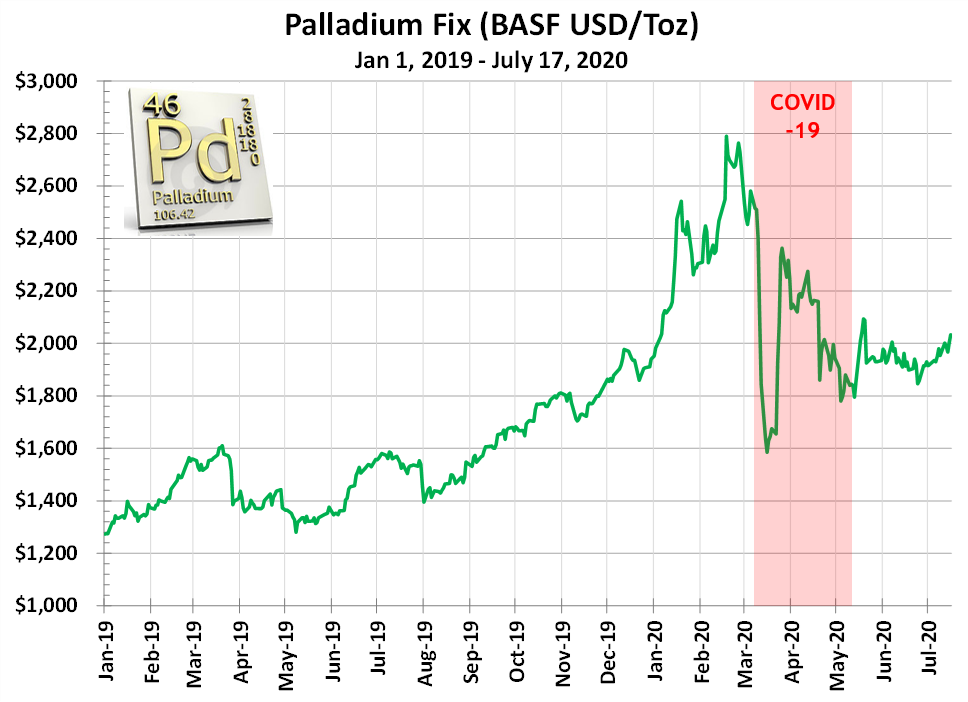

Palladium

Supply Highlights: Clearly COVID related impacts in 2020 will limit supply. Recent Nornickel diesel spill impacts on Q3 output are very unclear. Demand Highlights:

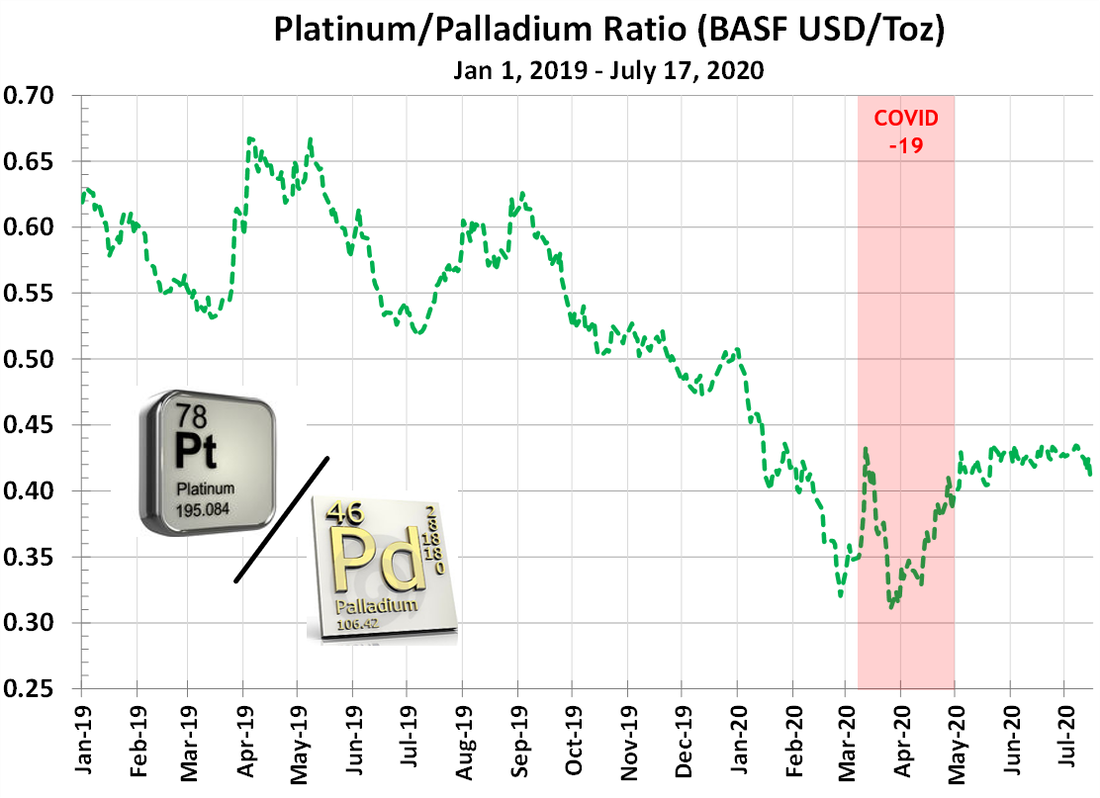

Platinum/Palladium Ratio

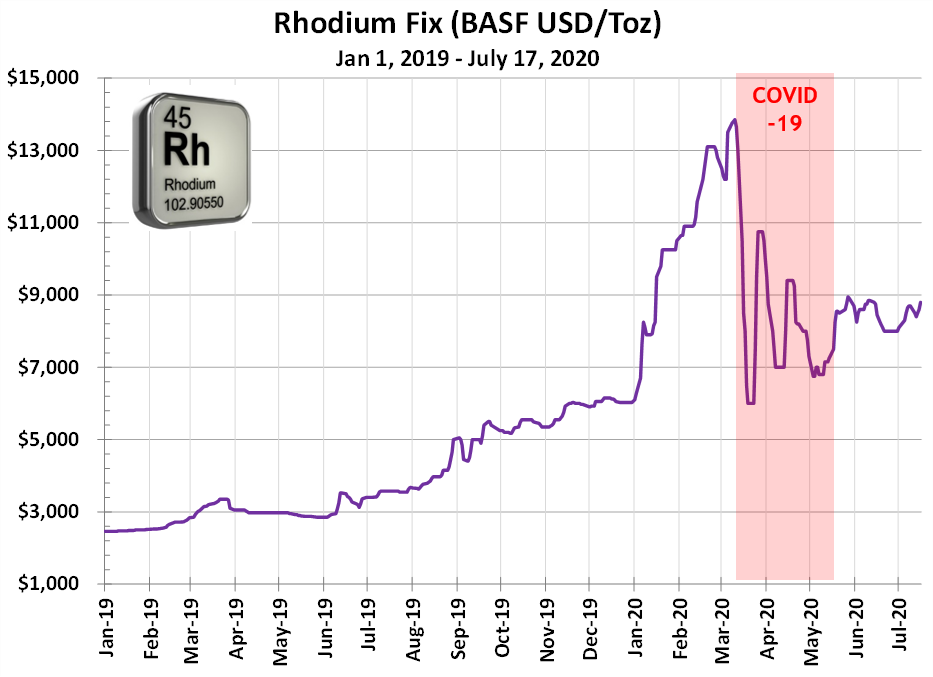

Rhodium

Supply Highlights: S. African PGM Western Limb mining declines dramatically hurt future mined supply. Demand Highlights –

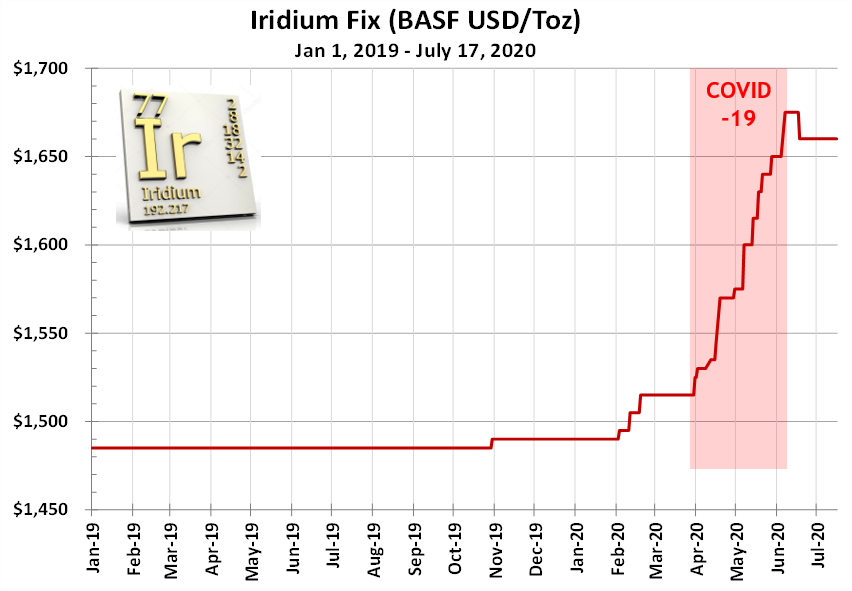

Iridium

Supply Highlights S. African PGM Western & Eastern Limb mining declines likely to reduce future mined supply. Near term continued COVID-19 mining disruptions will further impact Iridium supply. Demand Highlights – Electronics demand is strong: Crucibles for LED’s, OLED IrCl Materials, and SAW/BAW Filter demand will explode with 5G expansion.

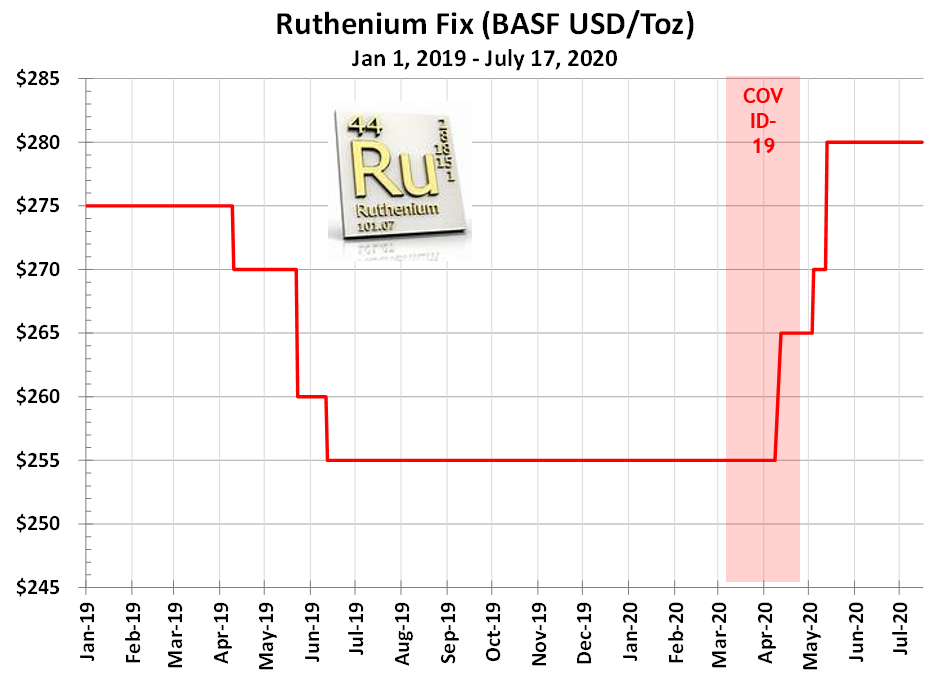

Ruthenium

Supply Highlights S. African PGM Western Limb mining declines dramatically hurt future mined supply. Demand Highlights –

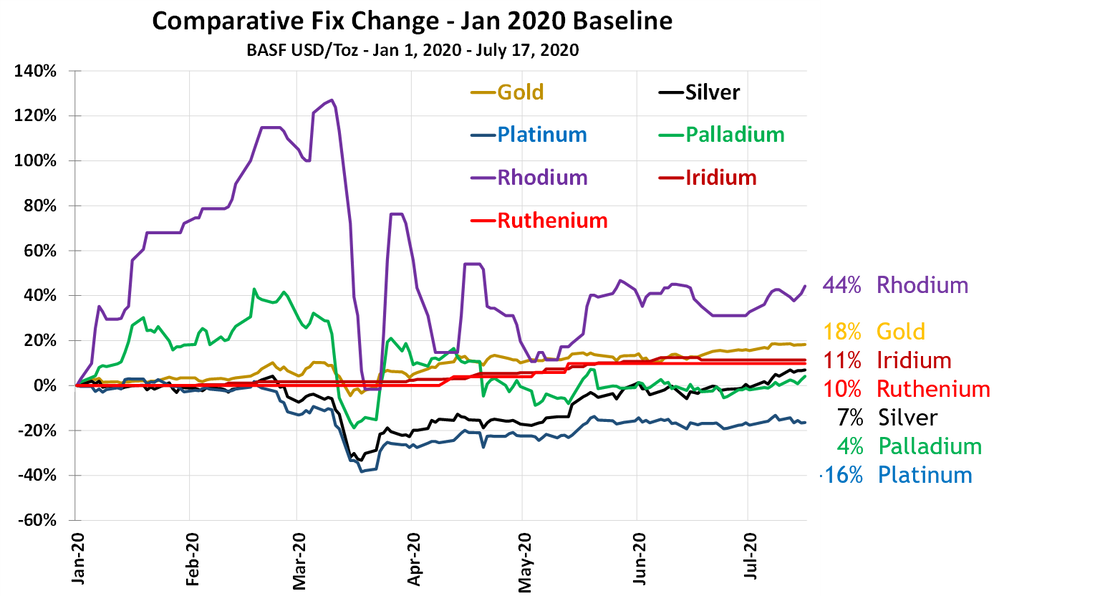

Precious Metals Basket 2020 Year To Date

2020 2nd Half Outlook

0 Comments

Leave a Reply. |

Author

Matt Watson, Precious Metals Commodity Management LLC Archives

November 2020

Categories |

RSS Feed

RSS Feed